By 2030 renewable energy sources such as solar and wind will cost a similar amount to fossils fuels such as coal and gas, thanks to falling technology costs, according to new forecasts.

By 2030 renewable energy sources such as solar and wind will cost a similar amount to fossils fuels such as coal and gas, thanks to falling technology costs, according to new forecasts released in the CO2CRC’s Australian Power Generation Technology (APGT) Report.

The report also shows that technology costs will fall faster under climate policies that limit the concentration of carbon dioxide in the atmosphere to 450 parts per million. (The current CO₂ concentration is around 400 parts per million).

While the practice of forecasting is often derided, with multi-billion dollar assets that can last 50 years or more, the electricity industry and the policy-makers, academics and stakeholders who study it have no choice but to get involved.

Updating the data

A key input to all energy crystal-ball gazing is the cost of generating electricity, and performance data. However the last comprehensive update of electricity generation costs was the then Bureau of Resource and Energy Economics’ Australian Energy Technology Assessment (AETA) in 2012 (followed by a minor update to selected data in 2013).

The lack of consistent up–to-date data disadvantages technologies such as solar photovoltaic power systems whose costs have been improving rapidly since then.

To avoid misrepresenting the possible future role of fast-moving technologies, many analysts have had to slowly abandon use of the old data and create their own more up-to-date estimates.

While diverse opinions are sometimes useful, a proliferation of inconsistent alternative cost data sets creates confusion for the industry as it makes each published study less comparable.

The delivery today of a new and consistent electricity cost data set therefore is an important and long awaited addition to the electricity industry’s toolkit. The new report was conducted over the July-November period and utilised an electricity industry reference group of around 40 organisations to provide input and feedback along the way.

Given the often heated debates in Australia around energy sources, the CO2CRC recognised that it is crucial that studies like these are conducted in an open and unbiased manner.

The report includes key “building block” data such as capital and operating costs, and performance data such as emissions intensity, water usage and expected usage rates.

The cost of energy

Whenever a new electricity generation technology cost and performance data set is created there is an opportunity to update our view of the relative competitiveness of each technology.

This is calculated using a measure called the Levelised Cost of Electricity (LCOE). The LCOE captures the average cost of producing electricity from a technology over its entire life. It allows the comparison of technologies with very different cost profiles, such as solar photovoltaic systems (high upfront cost, but very low running costs) and gas-fired generators (moderate upfront cost, but significant ongoing fuel and operation costs).

The LCOE is the best technology comparison measure available but is not without limitations. It cannot recognise the different roles technologies might play in an electricity system (e.g. such as supplying everyday, baseload power, or power for periods of peak demand) or the relative flexibility of plant to increase or decrease power supply as needed.

Accepting the limitations, the updated LCOE analysis finds that in 2015 natural gas combined cycle and supercritical pulverised coal (both black and brown) plants have the lowest LCOEs of the technologies covered in the study. Wind is the lowest cost large-scale renewable energy source, while rooftop solar panels are competitive with retail electricity prices.

It is interesting to note that all 2015 LCOE estimates are higher than the current wholesale price of electricity of around A$40 per Megawatt-hour. The reflects reduced demand in the electricity network, which is putting downward pressure on electricity prices.

By 2030 the LCOE ranges of both conventional coal and gas technologies as well as wind and large-scale solar converge to a common range of A$50 to A$100 per megawatt hour. This outcome is consistent with observations from many commentators noting that the continuing reductions in wind and solar photovoltaic costs must inevitably lead to an intersection with the costs of the existing mature technologies before too long.

Of course, equality in LCOE will not necessarily translate to an equal competitive position in electricity markets, given differences in the flexibility of renewable and conventional coal and gas plants (which LCOE does not capture as already noted).

Falling technology costs

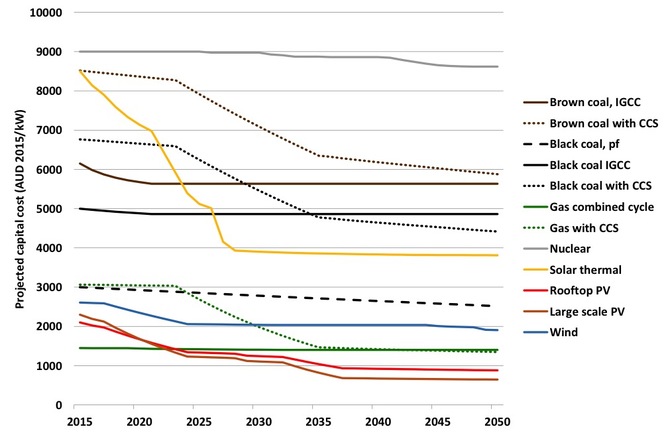

The convergence of conventional and renewable energy costs depends on the capital costs of these energy sources. These were modelled for the new report by CSIRO’s Global and Local Learning Model. This model is a relatively objective way of projecting costs based on historical learning rates. Learning rates show that for each doubling of installed capacity of an energy source, costs fall by a particular amount.

We can model these costs across different climate policies, as you can see in the chart below.

Projected electricity generation capital costs assuming a 550ppm consistent global carbon price signal CO2CRC

CSIRO’s projections included carbon price signals consistent with either concentration of 550 parts per million or 450 parts per million of greenhouse gas emissions. However, we found the total amount of cost reduction was fairly similar, but more accelerated in time, by approximately five years, in the 450 ppm case.

With the future policy environment of the electricity industry potentially becoming a little clearer after the COP21 meeting in Paris next week, the new report makes the job of understanding the role of different technologies in that future a little easier.

![]() Paul Graham, Chief economist, CSIRO energy, CSIRO

Paul Graham, Chief economist, CSIRO energy, CSIRO

This article was originally published on The Conversation. Read the original article.

16th December 2015 at 5:17 pm

Your article implies that the costs will converge ONLY if renewables have subsidies – as indicated when you mention so many ppm of CO2.

Is that correct?

2nd December 2015 at 1:53 pm

We need to realise that Solar is not a reliable source of energy and it has been proven (but denied) by the University on their very expensive Government paid for solar array. I have had this discussion with them (being an Engineer myself) and they promoted cumulative output and I insisted they advertise instantaneous instead. And they have a website showing the output to be looked at, example http://solar.uq.edu.au/user/reportPower.php?dts=2015-10-24&dtra=day showing that without storage backup, it is useless. I worked on a 1.2MW UPS system once and the battery room for it for a couple of hours backup was twice my house, So storage backup is not viable And I am happy to debate this with anyone

2nd December 2015 at 11:57 am

I seem to be missing something in the energy generation comparison debate. When the cost of coal based technologies becomes greater than that of alternative technologies then we all switch to the alternatives thus reducing the greenhouse gasses we pump into the atmosphere. If you consider say solar cell technologies, I have trouble finding articles that spell out how much greenhouse gas is produced in the life-cycle of a typical solar cell array. This includes the mining and processing of raw materials, manufacture and transportation etc. So when these comparisons are done (in the name “greenhouse gas reduction”) has the end-to-end greenhouse gas production of a technology been somehow attributed/converted to a cost (that is a dollar cost), that the average person in the street can understand? If this is so, does it only concern the production of CO2 or are there bi-products of these processes which are far more dangerous than CO2 that are not accounted for?

28th November 2015 at 11:32 am

Reliability of energy supply is most important, solar and wind energy being most inconsisitent. Peak load periods require full time maintainance of coal-fired generators as backup to supply energy at any instance, or during fluctuating load periods. Nuclear power seems the only practical alternative to coal. Solar and wind have the advantage in the bush or desert regions where normal power sources are unavailable.

27th November 2015 at 10:45 am

Has anyone looked at the social factors around a huge cohort of baby boomer’s approaching retirement and investing in rooftop solar as a way of improving their standard of living after their retirement? I know as I get nearer to retirement I am looking for ways to improve cash availability after retirement. In this scenario I am looking at what investments in renewable’s I can make just before retirement (Solar high upfront cost and low operational cost). This changes the economic drivers for me dramatically. After all solar panels have a life of around 25 years, you retire at 65 and the solar panels wear out when you do 🙂